As we move further into 2025, service companies are actively planning for the year ahead and seeking ways to stay ahead of the competition. This e-book delves deep into the factors that will shape the future—price outlook, M&A impacts, oilfield country tubular goods (OCTG) and pressure pumping. It’s an essential guide for navigating the complexities of tomorrow and securing a place at the forefront of the oilfield service sector in 2025.

Enverus Intelligence® Research, Inc., a subsidiary of Enverus, provides the Enverus Intelligence® | Research (EIR) products. See additional disclosures.

Research written by:

Mark Chapman, Principal Analyst Research, Enverus

Oil & Gas Research Team, Enverus Intelligence® Research

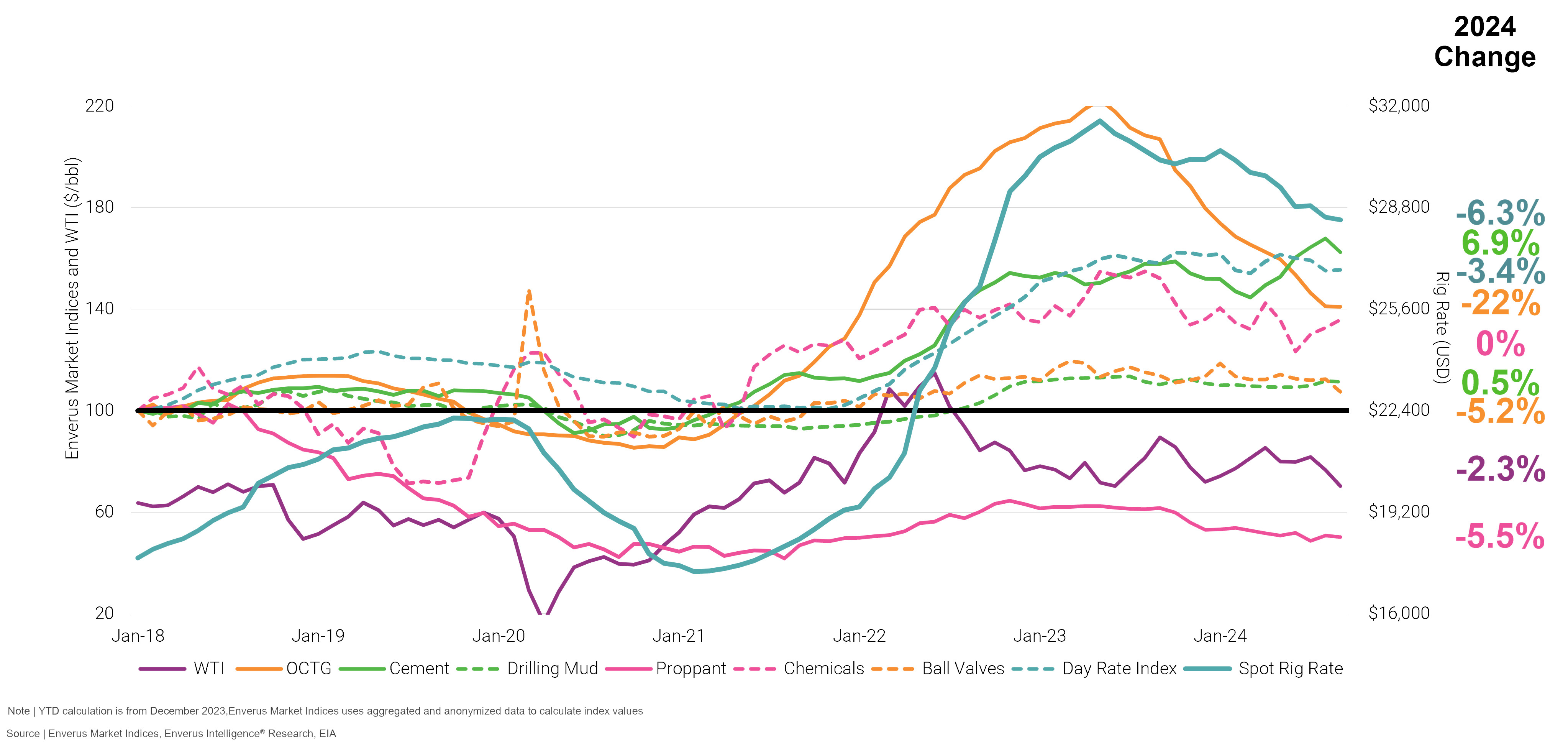

Despite record oil production in 2024 and an impending gas boom in 2025, the oilfield supply chain has had a rough couple of years. OCTG prices have dropped by as much as 50% from their peak, while sand prices have also declined. However, drilling mud and cement have been more stable, with prices flat and up 7%, respectively. Rising tides have not yet lifted all boats. But we view the tide is indeed turning for oilfield consumables, drilling and pressure pumping services with a bottoming of activity in 2H24. Let’s explore the market forces leading to reduced demand, the macro-outlook for oil and gas prices, and what to expect in 2025.

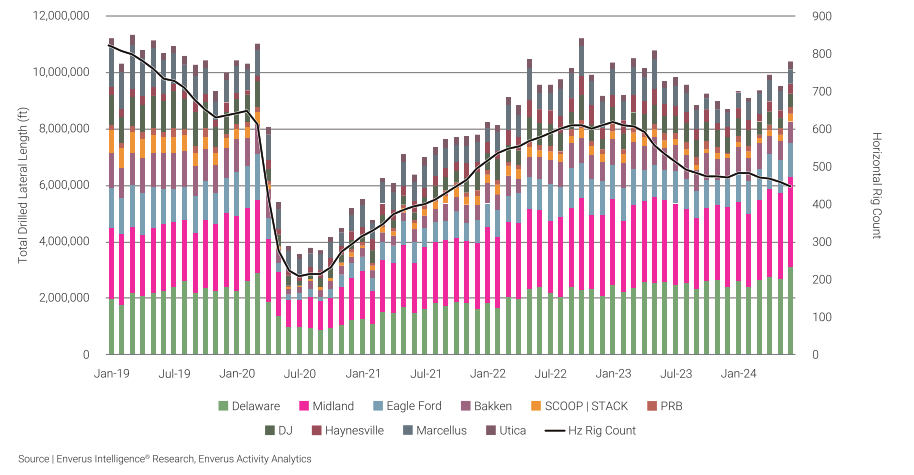

The wave of M&A in 2023 was driven by inventory hungry E&Ps buying privates who had an outsized portion of activity at the time as they try to prove up their acreage. The buyers desire to preserve inventory ended up laying down typically 20% of the acquired company’s rigs.

This consolidation has meant a greater portion of activity is in the hands of larger efficiency minded operators who leverage three-mile laterals and implement batch drilling and rig automation to yield a tremendous level of drilling efficiency never before seen in the industry. Pressure pumping operations are also more efficient, enabling by new state-of-the-art equipment capable of around the clock operations and requiring fewer frac fleets.

Enverus is defying the consensus with a more bullish $85 Brent base case. Demand wise, global oil consumption is set to increase by approximately one million barrels per day in 2025. Supply is expected to remain stable with OPEC’s winding down of cuts offset by members who have been outproducing their quotas. That being said, it’s the low levels of OECD stock inventories that are bolstering the $85 outlook (low $80 WTI) as inventory levels are historically correlated with oil prices, including the U.S. Strategic Petroleum Reserve which is about half empty.

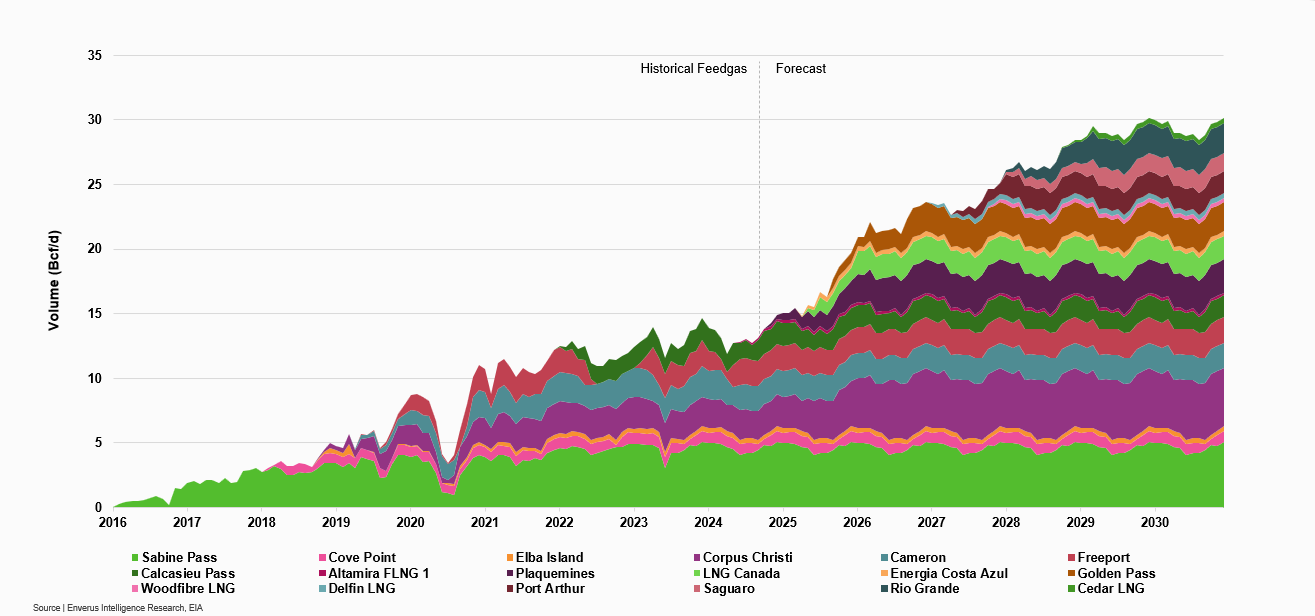

Up to 7 additional Bcf of LNG demand is expected for Gulf Coast and Canadian exports through 2026. Upstream and midstream are preparing for the impending gas price rebound by strategically holding acreage in the Haynesville and building up takeaway capacity. Low to negative Waha prices have been the curse of the Permian for the past few years, leading operators to either flare natural gas and take the regulatory hit or pay to have associated gas hauled away. Those days are coming to an end with the recently opened Matterhorn Express, up to 2.5 billion Bcf per day of takeaway capacity is now online with additional pipeline on the way, such as the Blackcomb and Gulf Coast Express Expansion pipelines. Paired with the completion of multiple LNG facilities in 2025 and 2026 on the Texas and Louisiana Gulf Coast as an outlet for the supply. We believe the Haynesville is the marginal gas play that will swing production depending on natural gas prices go in beyond 2025 and beyond.

Operators have managed to hit their production targets with 30% fewer rigs from 2022 to 2024, and this trend is expected to continue through 2026 with increasing productivity and decreasing rig count. However, utilization remains strong overall for 1,500 horsepower rigs, with approximately 80% utilization over the past twelve months. Super-spec rigs, which are almost exclusively under contract, will continue to command higher rates due to their ability to drill three-mile laterals and achieve the efficiency operators seek.

In 2024, drilling rates declined approximately 6% on contracts and 3.4% for daily rig rentals. As we move further into 2025, we anticipate contract prices to align more closely with spot rental rates following the tendering season and the start of new contracts at the beginning of the year. Although the number of private E&Ps spudding new wells has decreased, this number is expected to rise in 2025 as private operators assemble positions in tier-two acreage and non-core assets divested by public E&Ps.

Looking ahead, the oilfield service sector is set for significant changes. With the anticipated rebound in oil and gas prices, driven by strategic investments and technological advancements, companies can benefit from new market conditions. The outlook for Brent and the growing LNG export market suggests a path to higher margins. Now is the time for service companies to position themselves at the forefront of this dynamic landscape, leveraging insights and innovations to navigate the complexities of tomorrow. For a deeper dive into the opportunities and price outlook for 2025, speak to an expert today.

Discover

About Enverus

Resources

Follow Us

© Copyright 2025 All data and information are provided “as is”.