Global commodity markets will be pushed and pulled in multiple dimensions with a trifecta of change in 2025: a second Trump presidency and a Republican majority in both the house and senate. These shifting political winds will shape supply, demand and pricing with a new federal administration resetting policies on trade, energy and foreign relations. Donald Trump’s first term demonstrated a willingness to bolster U.S. energy independence, promoting oil and gas development and challenging international agreements aimed at curbing emissions. These policies, while beneficial for domestic producers, introduced volatility into global markets.

Get the data behind this e-book to power your 2025 strategy. Let’s connect to discuss your free trial and how our insights can drive your decisions.

Research written by:

Tamas Varga, analyst at PVM

Victor Laurent, Head of product, Parameta Solutions

This report explores the potential impacts of a second Trump presidency on oil markets, emphasizing the nexus between domestic and international policies. We’ll examine how Trump’s economic strategies, including tariffs and industrial incentives, may influence energy demand and market stability. Explore the likely changes to energy policies, such as deregulation, increased production and shifts in renewable energy commitments. This report will also delve into foreign policy, analyzing how geopolitical maneuvers could alter oil trade dynamics and set the U.S. up to achieve greater energy independence with less volatility.

By unpacking the likely policy directions of a Trump administration, Enverus hopes to provide valuable insights for market participants to better anticipate changes, mitigate risks and capitalize on opportunities in an energy landscape that is poised for rapid change.

Economic policy under a second Trump administration would likely prioritize American industry, aiming to reduce reliance on foreign goods and energy. Trump’s proposed tariffs, such as a 10% general import tax and a 60% targeted trade action against Chinese imports, signal an intensified focus on economic protectionism. While such measures aim to bolster domestic manufacturing and energy consumption, they could inadvertently raise costs for consumers and businesses. Higher costs could reduce disposable income, reducing consumer spending on fuel and lowering oil demand domestically.

Broad tariffs have the potential to disrupt global supply chains, creating uncertainty in oil markets. During Trump’s first term, elevated trade tensions with China generated volatility in energy pricing as markets reacted to shifts in industrial activity and demand. The World Trade Organization criticized such tariffs as a lose-lose scenario, highlighting the risks of global economic slowdown – a situation that typically reduces energy consumption.

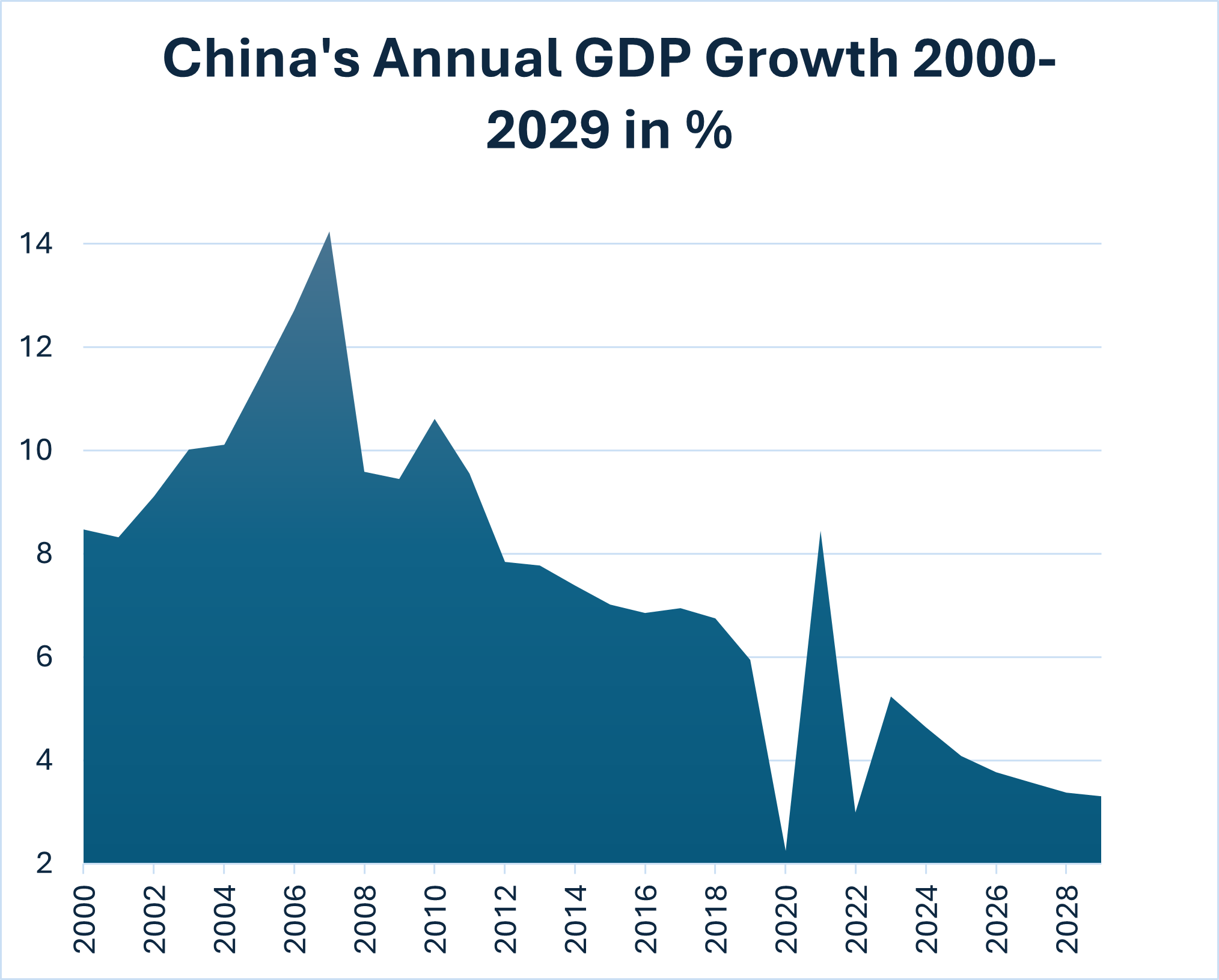

Figure 1: Historical and forecasted Chinese gross domestic product

Adding fuel to the fire, China’s GDP is on the glidepath down, creating fierce competition for economic growth. Targeted trade action, i.e., tariffs, may only paint China into a corner in terms of optionality, ratcheting up geopolitical risks to new levels.

In this environment, market participants must consider potential economic disruptions, as reduced industrial output in major economies like China and the U.S. could suppress global oil demand while introducing price volatility. At the same time, Trump’s focus on domestic energy production could reshape global trade, further influencing markets.

Energy policy under a second Trump term would likely continue to emphasize deregulation and expansion of oil and gas production. Trump’s first administration set the tone by rolling back environmental regulations (e.g., Quad O) and his reelection could see even more aggressive moves. This includes halting new LNG export permits to prioritize domestic energy needs and scrapping the Waste Emissions Charge that would hit balance sheets in 2025 based on 2024 reporting. The net effect would reduce costs and emissions liability, encouraging producers to increase output and increase margins.

A second Trump term would also likely push for increased drilling, both offshore and on federal lands. These efforts align with Trump’s broader strategy to achieve energy independence, reduce reliance on OPEC and position the U.S. as a dominant global oil supplier.

During his first term, shale oil production reached unprecedented levels, contributing to an oversupply that influenced global pricing. A continuation of this strategy could put downward pressure on oil prices, creating challenges for high-cost producers globally.

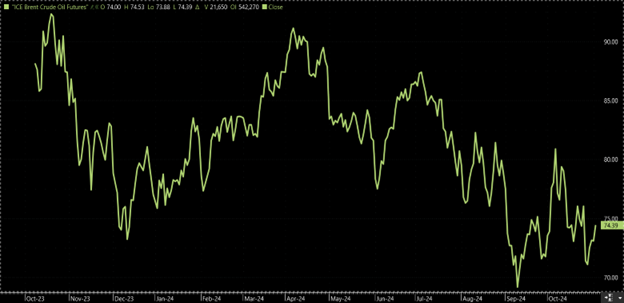

Figure 2: Enverus MarketView® shows gasoline prices during first Trump term and Biden’s presidency. The MarketView Platform provides instant connectivity across devices, delivering mission-critical alerts and forecasting on pricing, risk, and end-of-day functions.

Trump is likely to remain keenly aware of the negative correlation between gasoline prices and presidential approval as he takes office. Comparing his first term to Biden’s only term, we can expect to see lower gasoline prices again over the next four years. Consequently, stabilizing gasoline prices will likely remain central to Trump’s energy agenda. By increasing domestic supply, Trump may seek to keep retail prices low, acknowledging their political significance.

Trump left the Strategic Petroleum Reserve (SPR) about half empty (or half full depending on your optimism) after his first term. Replenishing the SPR may become a focus although drawing it down to stabilize gasoline prices like his predecessor did is not likely in his second term.

Trump’s policy changes could further slow the energy transition. By prioritizing oil and gas and potentially revoking subsidies for renewable energy and electric vehicles (EVs), his administration may slow down progress toward reducing global oil dependence. For market participants, this creates opportunities to capitalize on continued demand for traditional energy sources amidst a slower-than-expected transition to renewables.

Trump’s foreign policy, characterized by unilateralism and an “America First” posture, could introduce significant changes to global oil markets. A second term would likely see renewed efforts to resolve international conflicts, albeit with strategies that may prioritize U.S. interests over global stability.

Figure 3: Enverus MarketView | Russian oil output not likely to increase following an end to the Ukraine war

For instance, Trump’s promise to end the Ukraine war within a day showcases his willingness to push for rapid resolutions, even if they involve significant tradeoffs. Critics argue that such actions could exacerbate geopolitical tensions, triggering short-term oil price spikes. And a swift resolution might not help the Russian oil industry reclaim its Western customers, as long-term geopolitical tensions and sanctions could persist for years.

Figure 4: Enverus MarketView | Brent crude oil volatility as Israel’s conflict continues in the Middle East

The Middle East will remain a key focus for the new administration. Trump’s “maximum pressure” strategy, characterized by withdrawal from the Iranian nuclear deal and reinstating sanctions, has previously elevated geopolitical risk premiums in oil pricing. Trump may double down on this approach, maintaining a hardline stance against Iran. This could result in increased volatility as markets respond to a potential supply shock from one of the region’s largest producers.

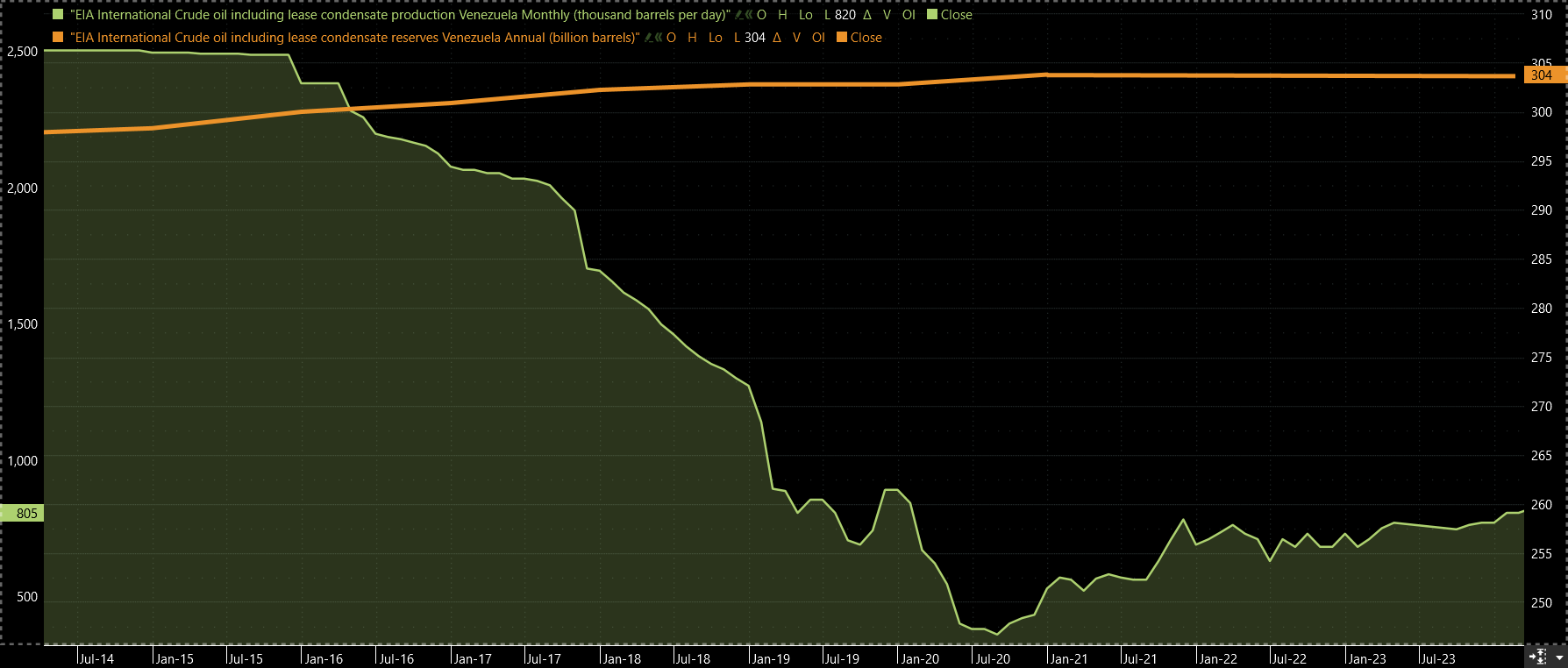

Figure 5: Enverus MarketView | Impact of sanctions on Venezuelan production started day one of Trump's first term

Venezuela’s role in the global oil market may also evolve under a second Trump term. While his first administration imposed strict sanctions, a renewed focus on countering OPEC’s influence could lead to attempts at rebuilding U.S.-Venezuela relations. Such efforts could unlock new supplies, stabilizing global markets and reducing dependence on Middle Eastern oil. However, rebuilding Venezuela’s production capacity would require significant investments in both diplomacy and capital.

Trump has long criticized OPEC and continuously pushed for measures to increase U.S. energy independence. Although never passed, the NOPEC bill took aim at the cartel’s monopoly and outright price manipulation. The risk and reward calculus of such legislation is not fully embraced by the energy industry; however, we may see similar bills in the coming years that may have more of a chance of passing with a Republican majority in the house and senate, creating potential for supply shocks.

Market participants should also consider the divergence in oil demand estimates between OPEC, which tends to talk up its book and the International Energy Agency (IEA). Trump has argued that IEA’s overly bullish view of the energy transition has undermined investment in fossil fuels and, in turn, energy security.

Energy Independence vs. Energy Transition

Achieving energy independence has been a cornerstone of Trump’s energy policy. U.S. crude oil production hit record levels during his first term and a second term could sustain this trajectory. Current production rates exceed 13.5 million barrels per day, with the U.S. accounting for 20% of global demand.

Figure 6: Enverus MarketView | The trajectory of U.S. production output

However, peak production is expected by 2030 and slowing growth may require strategic planning to maintain dominance. Here, the U.S. oil and gas industry continues to sharpen its competitive edge through advancements in drilling, completion and production technologies as well as economies of scale and capital efficiencies created through mergers and acquisitions.

The rise of EVs and renewable energy sources presents a challenge to the oil industry. Although EV adoption has grown, with more than 1.4 million new registrations in 2023, the transition away from oil and gas has been slower than anticipated. Trump’s potential repeal of the current $7,500 EV tax credit could further delay this shift, ensuring continued demand for oil in the near term.

The energy transition lags despite growing numbers. Balancing short-term gains in oil and gas production with long-term sustainability will remain a critical challenge. For market participants, this dynamic creates opportunities to leverage sustained demand for traditional energy while preparing for eventual shifts toward renewables.

Key Takeaways

A second Trump term holds profound implications for global oil markets, with policies likely to prioritize U.S. energy independence, expand oil and gas production and disrupt international trade dynamics. While these strategies could benefit domestic producers and consumers, they also introduce volatility into global markets, creating both risks and opportunities. Understanding these potential shifts is essential for navigating an increasingly complex energy landscape, where geopolitical moves and economic policies play pivotal roles in shaping supply, demand and pricing.

Get the data behind this e-book to power your 2025 strategy. Let’s connect to discuss your MarketView free trial and how our insights can drive your decisions.

Schedule a Meeting

Let’s get started!

We’ll follow up right away to show you a quick product tour.

Let’s get started!

We’ll follow up right away to show you a quick product tour.