Are we seeing the first little clawbacks of price creep back in drilling and completing new wells? We don’t have a lot of evidence yet, but a few signs of increasing prices for oilfield services (OFS) are appearing on the horizon. For example, Devon Energy said that per unit expenses are up by ~5% in the quarter as a result of severe winter weather in Texas. We know the February freeze generated some supply scarcity after temporary shutdowns across the state of sand mining, chemical blending and even chemical feedstock from the refineries. This capacity was not down for long, days to a week in most cases, but this lack of production caused a drawdown on supplies of consumables.

The temporary shortages will work themselves out, but let’s consider recent tough times for OFS companies. Last year they had to turn inventory into cash to survive a sharp drop in drilling and completion activity after oil prices crashed; now they are expected to turn cash back into inventory when service prices are at all-time lows but those for raw materials (steel, diesel and chemical feedstock) costs are increasing. It is difficult for OFS firms to sink even more cash into restarting facilities and refurbishing equipment in storage without a guarantee of stronger pricing. Additionally, staff shortages could also push up prices. While some oilfield hands that will always be oilfield hands, a truck driver can change industries to one that is less cyclical, meaning OFS companies may have to pay up to attract back workers.

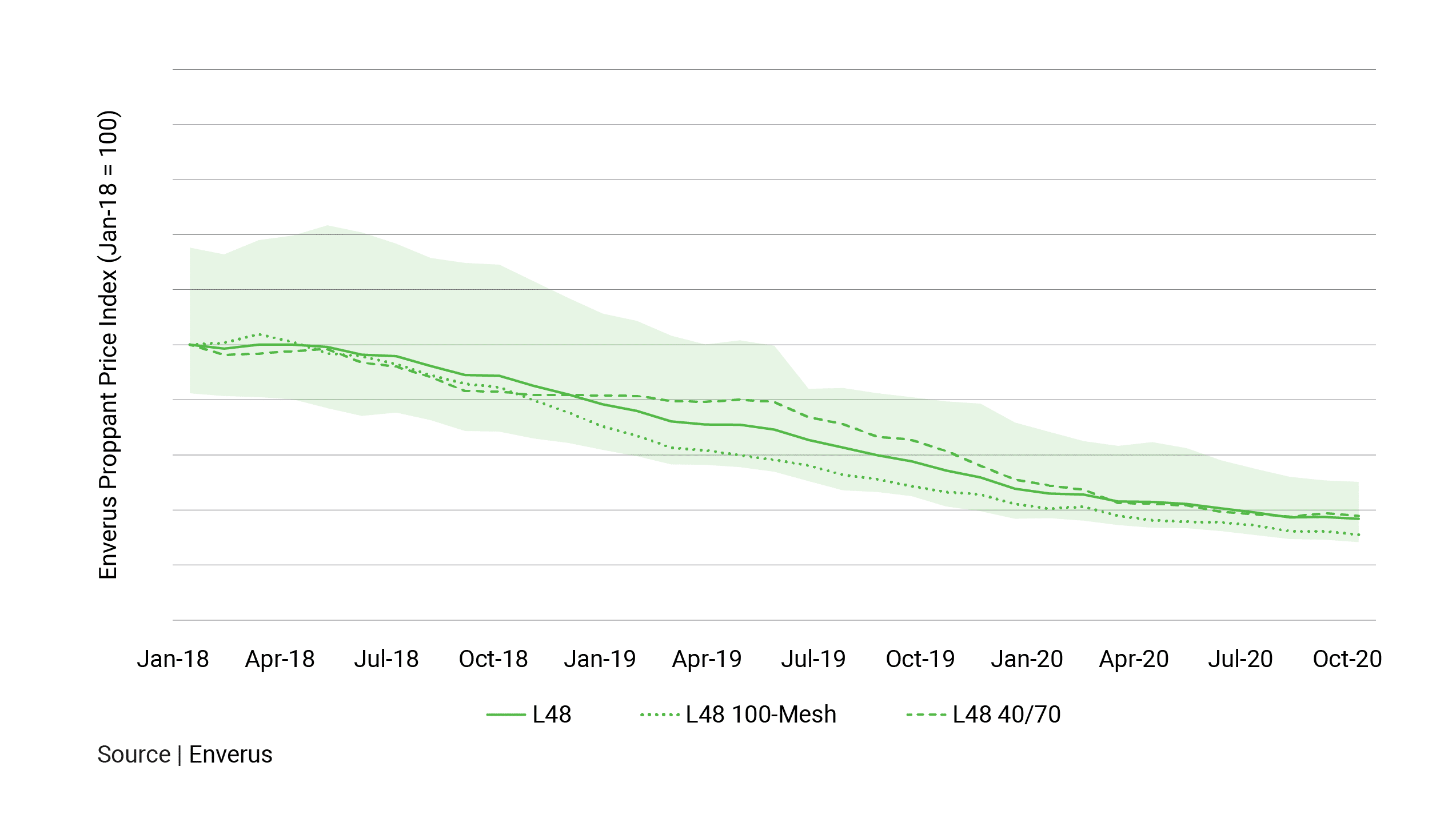

The OFS sector gained new efficiencies and new abilities to work lean throughout the 2020 downturn, lessons that will stick around for a while. We will be looking at our OpenInsights Market Indices (Figure 1) for data on how the various factors play out. What do you think will happen?

FIGURE 1 | U.S. Fracture Sand Index