Last month, Ian Nieboer from our Enverus Intelligence team teamed up with Tim Hard, Senior Vice President of Energy Transition from Argus, to provide expert insights on the market dynamics of hydrogen, including:

- Where emerging market opportunities are for hydrogen

- How to make market assessments using MarketView

- Best practices for energy trading and risk management

Missed the live discussion? Watch the on-demand webinar to hear all the insights and to learn how Enverus Trading & Risk solutions can help ensure you have the accurate and timely data you need to act.

During the webinar, we received a number of questions from the audience and wanted to share some of those questions and answers here. Thank you to Tim and Ian for keeping the conversation going!

Q: Europe looks set to lead the new hydrogen economy. What differences between Europe, the U.S. and Asia stand out to you?

A: The U.S. is the most generous and loosest in rule stringency. The EU will be offering less and aim to stipulate more. Asia is problematic as Australia is low-balling the supply support funding, while Japan and Korea, though large individual economies, lack the EU/U.S. heft, nor have they joined policy up between them. Yet.

Q: What do you see for competing technologies that could impair or stop that launch for hydrogen? Carbon capture, methane pyrolysis?

A: The issue with methane pyrolysis is that technology is not there yet, and probably won’t be there until 2030, and there are a lot of assumptions as to what natural gas is going to do up to that point. Carbon capture is important, it is going to be used. Is it going to negate the need for hydrogen molecules, no? It is just not economic, and we need solutions now.

Q: How do you see costs impacting the development of the hydrogen economy?

A: It is costly at the moment, but cost will fall as scale increases. Every time there is a change to something else, cost is brought up. The cost is an issue, but the need is there.

Q: Are there catalysts on the horizon that are a launching pad on the demand side?

A: On the European side we have seen SAF being injected into mandates. It’s only electric going forward and you have two options electric vehicles (EV) or fuel cell electric vehicles (FCEV) which are powered by hydrogen, so you are starting to see those mandates coming through.

Q: Is the industry developing consensus on the which investment structures are best suited to hydrogen development? What does that look like?

A: Developers are strongly pushing to ensure offtake agreements are tied up (fully for stage 1s), before progressing to FID.

Q: What lessons should U.S. developers of hydrogen take from Europe, elsewhere?

A: Simple is best. Developers crave certainty before spades hit ground. Otherwise, I think it may be the other way round. The U.S. could take a leaf out of Europe’s book and look to carbon disincentives (taxes), as its northern neighbor Canada is doing.

Q: Is it reasonable to think that hydrogen will fuel more than 5% of the btu content a modern 500 MW CC plant produces?

A: Yes. Peaker plants need to continue to avoid intermittency problems and their co-firing rates should continue to rise.

Q: The shipping industry has reduced oil spills, but they are not perfect. How do you assess the risk of ammonia spills as a shipping fuel?

A: High. The industry has a stellar record, but size increasing by a factor of five increases risk of accidents beyond that factor. More of a concern is NH3 as a vector. A marine fuel spill is necessarily smaller scale than a cargo travelling Aus-NE Asia, the most biodiverse marine corridor globally.

Q: Do you believe that Brazil has space on this H2 opportunities?

A: Massive, undoubtedly. Low cost, huge land mass, great RE profiles.

Q: The electrolyser capacity mentioned, is it single stack?

A: Argus model in 1MW stack size for PEM (in 100MW total scale) and in 5MW for ALK.

Q: What are the key factors to reduce the H2 cost?

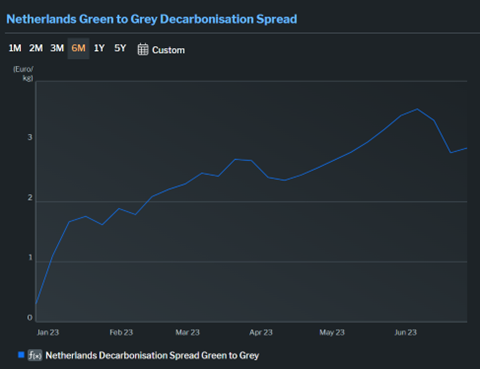

A: Cheap renewable energy ‘in’ to electrolysers via levelized cost of electricity (LCOE) is a huge driver for green hydrogen, while cheap gas/coal achieves the same for blue. As gas prices have fallen faster than LCOE, the cost differential between ‘renewable vs fossil’ has really opened, as below.

Carbon costs will further incentivize the switch from grey to blue and green – albeit there’s likely less room to run in the EU than in APAC/ME/ROW. The U.S. has effectively put a price of $85/t of CO2 in credits, which is within striking distance of EU C02 costs.

Watch the on-demand webinar to see the full conversation and learn more.

Fill out the form to speak to an Energy Transition expert, and learn more about the featured MarketView solutions.