Driven by goals in decarbonization, energy security and industrial competitiveness, Japan aims to integrate low-carbon hydrogen into its energy mix. Due to high costs and limited renewable energy capacity domestically, the country is actively investing in global hydrogen supply chains to address these challenges. Japan is financing production, transportation and infrastructure projects around the world to strengthen its hydrogen supply chains.

To accelerate hydrogen adoption and tackle cost barriers, Japan enacted the Hydrogen Society Promotion Act Oct. 23, 2024, dedicating 3 trillion yen ($20 billion) to establish a low-carbon hydrogen supply chain. Japan became the first country to publish a national hydrogen strategy in 2017. Since then, several nations have followed suit, with some even surpassing Japan in certain areas of hydrogen integration into their economies.

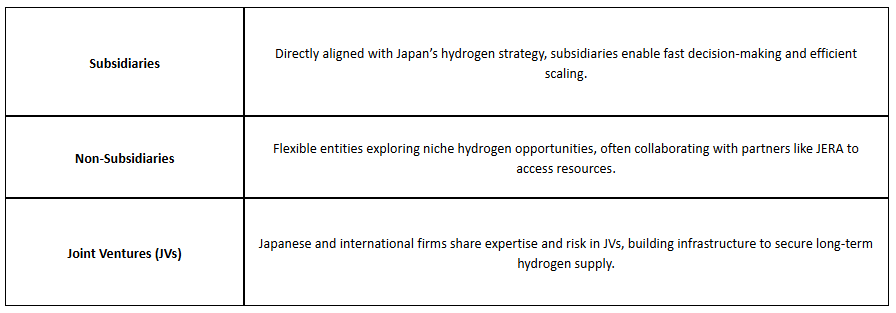

Organizational Structures in Japan’s Hydrogen Strategy

Understanding Japan’s use of subsidiaries, non-subsidiaries and joint ventures is critical to grasping how the country strategically organizes its hydrogen projects, both domestically and internationally. Each structure leverages specific strengths—such as alignment with national priorities, operational flexibility and shared expertise—that enable Japan to scale hydrogen initiatives effectively and navigate the complexities of global partnerships.

Japanese Partnerships & Investments in Overseas Blue & Green H2 Projects

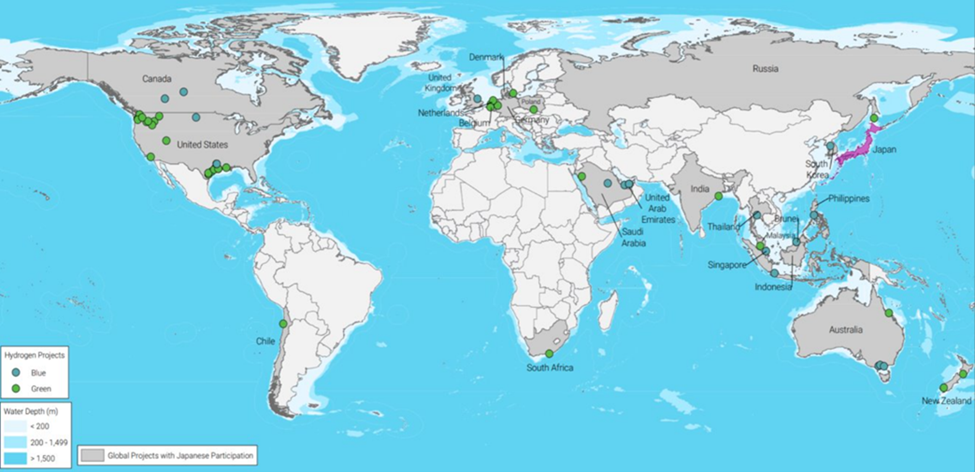

Japanese companies have partnered in more than 40 clean hydrogen projects worldwide, with a focus on North America, Europe, Australia, Southeast Asia and the Middle East. Japan’s strategy aims to diversify and manage risk by prioritizing asset quality, regional incentives and funding and transportation logistics.

Map of Japanese partnerships and investments in global clean (blue and green) hydrogen projects

Regional Analysis of Clean Hydrogen Production Opportunities

North America – The U.S. and Canada offers access to abundant low-cost resources and lucrative incentives which significantly benefits low-cost clean hydrogen production. However, its distance from Japan challenges logistics.

Europe – Limited, high-cost resources and the region’s distance from Japan diminish its appeal for hydrogen production. However, substantial funding mechanisms can enhance economic viability, provided developers secure access to the limited funding available.

Australia – Abundant low-cost resources and close proximity to Japan favor Australasian projects, with government funding available to support them on a project-by-project basis.

Middle East – The Middle East presents strong H2 investment potential, leveraging a strategic export position. However, Japanese firms must partner with state-backed enterprises, limiting autonomy but securing market access.

Southeast Asia – Despite limited government support, the region’s gas resources and low-cost center for blue hydrogen make it a promising prospect, with its proximity to Japan further enhancing its appeal for export.

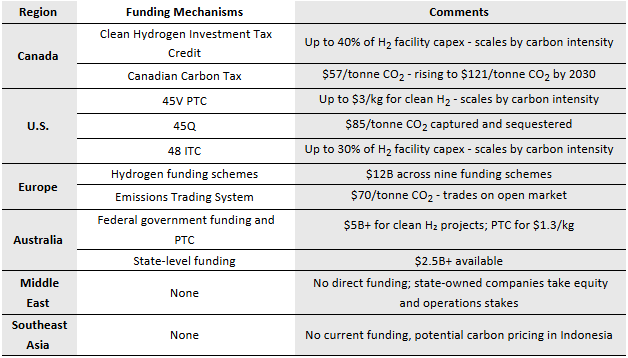

Regional Incentives and Funding Mechanisms for Clean Hydrogen

Note | All prices in USD. EU to USD exchange rate of $1.09/€. CAD to USD exchange rate of 1.40 CAD/USD. AUS to USD exchange rate of $0.66/AU$.

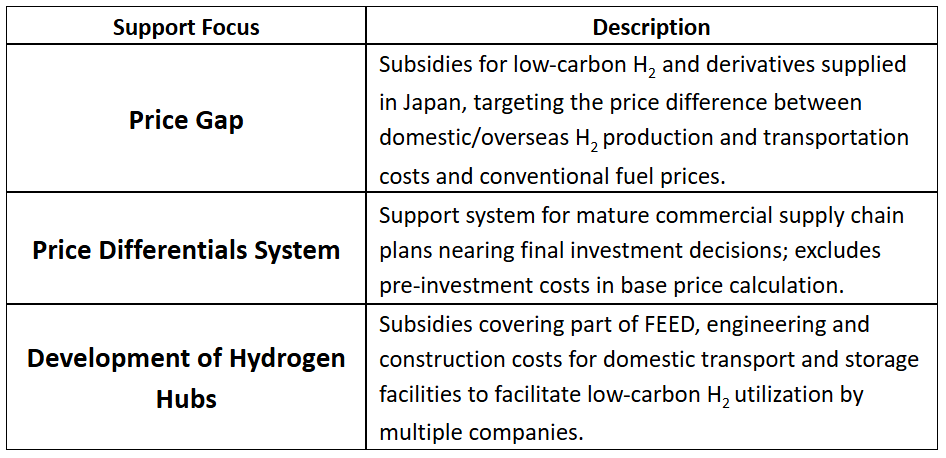

Government-Driven Support Mechanisms for Low-Carbon Hydrogen

The Ministry of Economy, Trade and Industry (METI) has appointed the Japan Energy and Metals National Corporation (JOGMEC) to oversee “support focusing on the price gap” and “support for the development of hydrogen hubs.” JOGMEC is responsible for facilitating low-carbon hydrogen supply and hub development. An overview of each support measures is as follows:

Suppliers producing or importing low-carbon hydrogen into Japan can apply for subsidies, though foreign producers cannot apply directly due to customs law. Applicants must submit a joint plan with end-users, specifying that supply will begin by FY2030, continue for at least 15 years (with an optional 10-year extension) and detail capital investment or innovation commitments from end-users.

Japan’s subsidy system also addresses the price gap, covering the difference between low-carbon hydrogen (base price) and conventional fuel costs (reference price) for certified suppliers to ensure continuous supply. Certified businesses receive support through JOGMEC if they meet METI’s standards, which require low-carbon hydrogen to significantly reduce CO₂ emissions and adhere to international guidelines and METI-specific requirements.

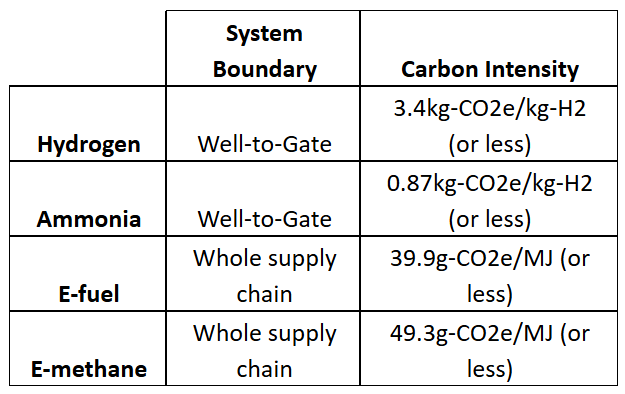

Under the Act, “low-carbon hydrogen” refers to hydrogen and its compounds that meet METI’s specified standards, emit significantly less carbon dioxide during production and contribute to CO₂ reduction in Japan, based on international emissions guidelines and additional METI requirements.

These values are presented as 70% lower than those for gray hydrogen and gray ammonia produced from natural gas (i.e., about 30% of which is emitted) and thus allows blue hydrogen and blue ammonia projects.

Table 1 – Carbon intensity standards for alternative fuels across supply chains Source – METI paper published June 7, 2024 (https://www.meti.go.jp/shinqikai/enecho/shoene_shinene/suiso_seisaku/pdf/014_01_00.pdf)

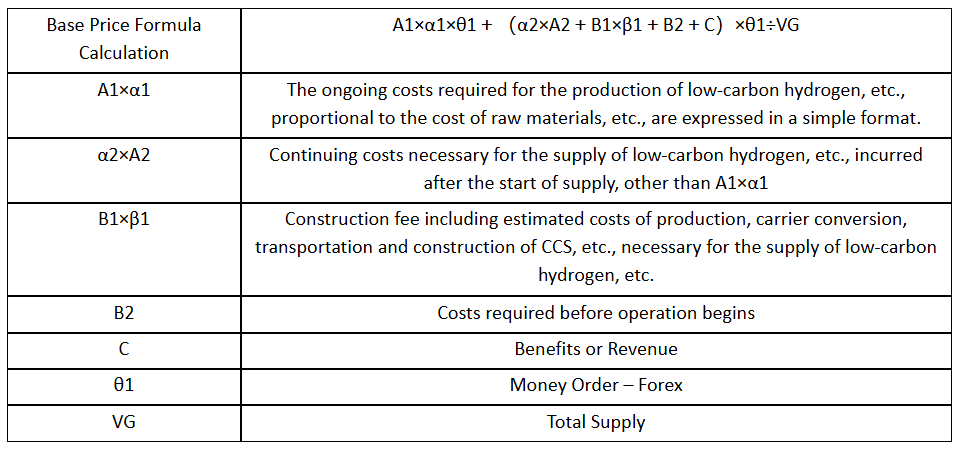

The base price formula (table below) calculates the cost of low-carbon hydrogen by accounting for ongoing production costs, continuing supply costs, construction fees and benefits or revenues, adjusted for currency exchange rates and total supply volume.

Table 2 – Base Price calculation components for low-carbon hydrogen supply Source – METI paper published Oct. 23, 2024 (https://www.jogmec.go.jp/content/300391803.pdf)

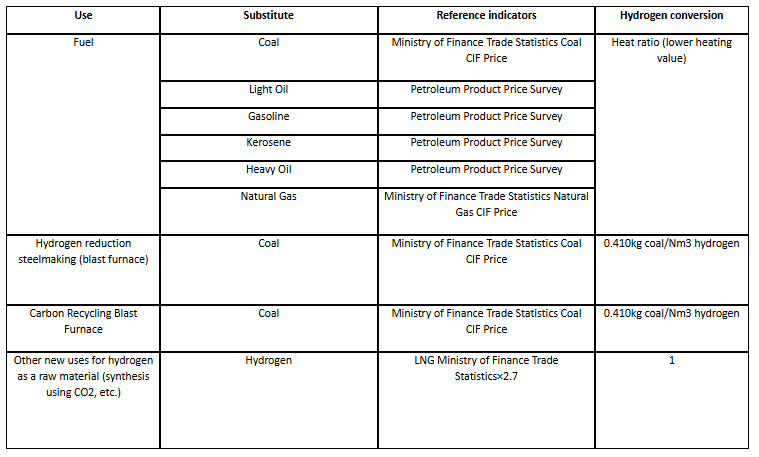

Table 3 (below) provides reference price indexes and conversion rates used in calculating hydrogen-related costs. It includes standard indicators and conversion factors for various fuels and hydrogen applications, enabling consistent cost assessments across different uses.

Table 3 – Reference price index and hydrogen conversion Source – METI paper published Oct. 23, 2024 (https://www.jogmec.go.jp/content/300391803.pdf)

Japan’s proactive approach to developing a global hydrogen economy, via investments in global hydrogen supply chains, balances domestic limitations with strategic international partnerships. By leveraging a mix of funding mechanisms, organizational structures and targeted de-risked regional investments, Japan is establishing a strong foundation for sustainable, low-carbon energy security and industrial competitiveness. As global competition intensifies, Japan’s success will depend on its ability to quickly adapt and scale its hydrogen strategies in response to evolving economic, technological and environmental challenges.

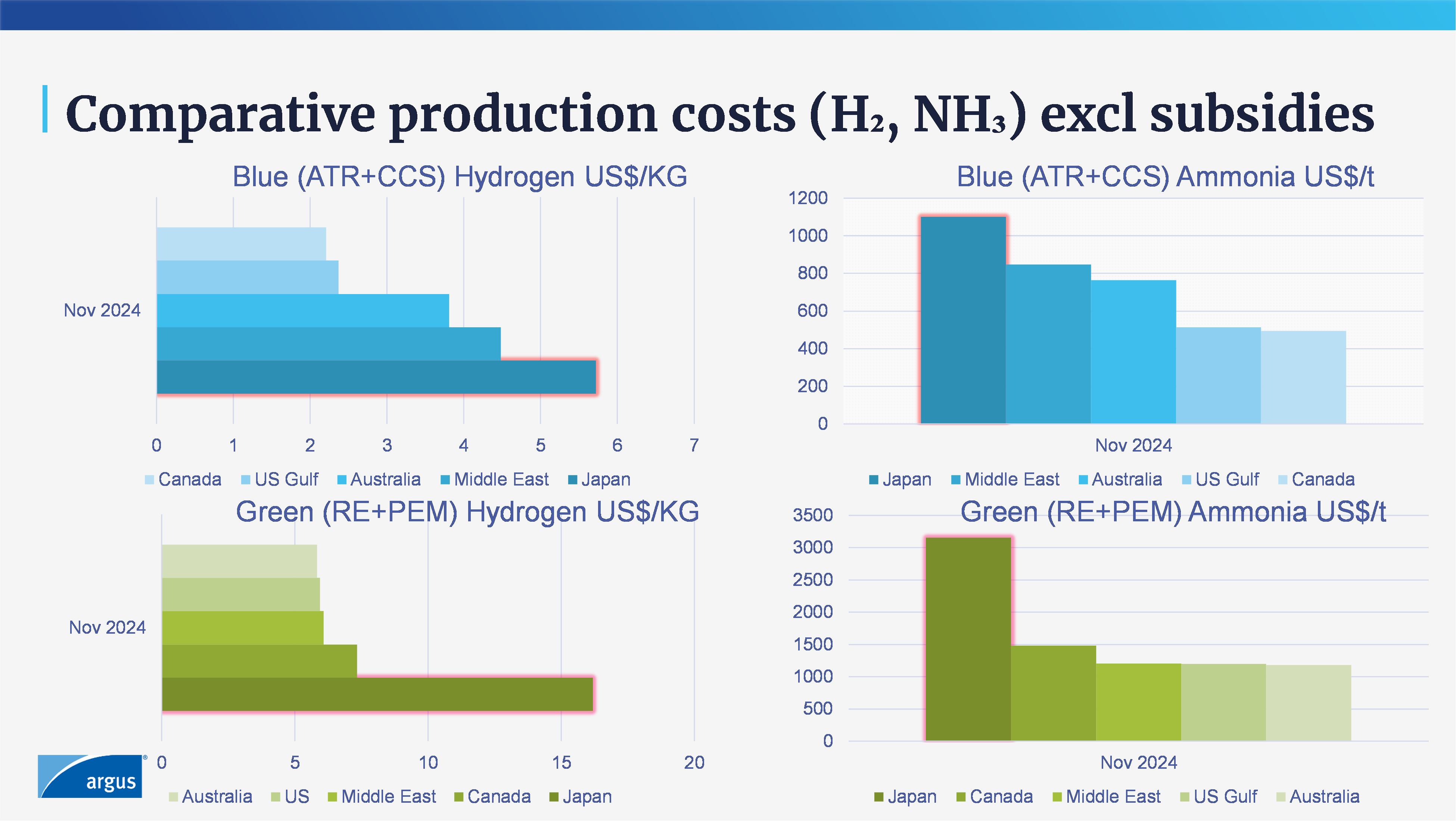

So, how does Japan’s high-level approach to sectoral development mesh with its practical comparative position for production economics? The country’s historical position of energy import dependence has translated into a soft approach of developing enduring relationships with exporting nations and a commercial approach of foreign direct investment (FDI) into projects. The emerging low-carbon supply chain is being approached in the same manner.

The bar charts on the left-hand side show domestic hydrogen production costs in germane locations noted in [table 2], excluding subsidies. Japanese blue production costs reflect both the country’s (high cost) position at the end of energy supply chains and poor carbon capture and storage (CCS) economics. It is similarly disadvantaged by a high levelized cost of electricity from renewable energy for electrolytic ‘green’ hydrogen.

While noting the large differential between renewable and fossil-source hydrogen, in both cases Japan is at a significant cost disadvantage to elsewhere.

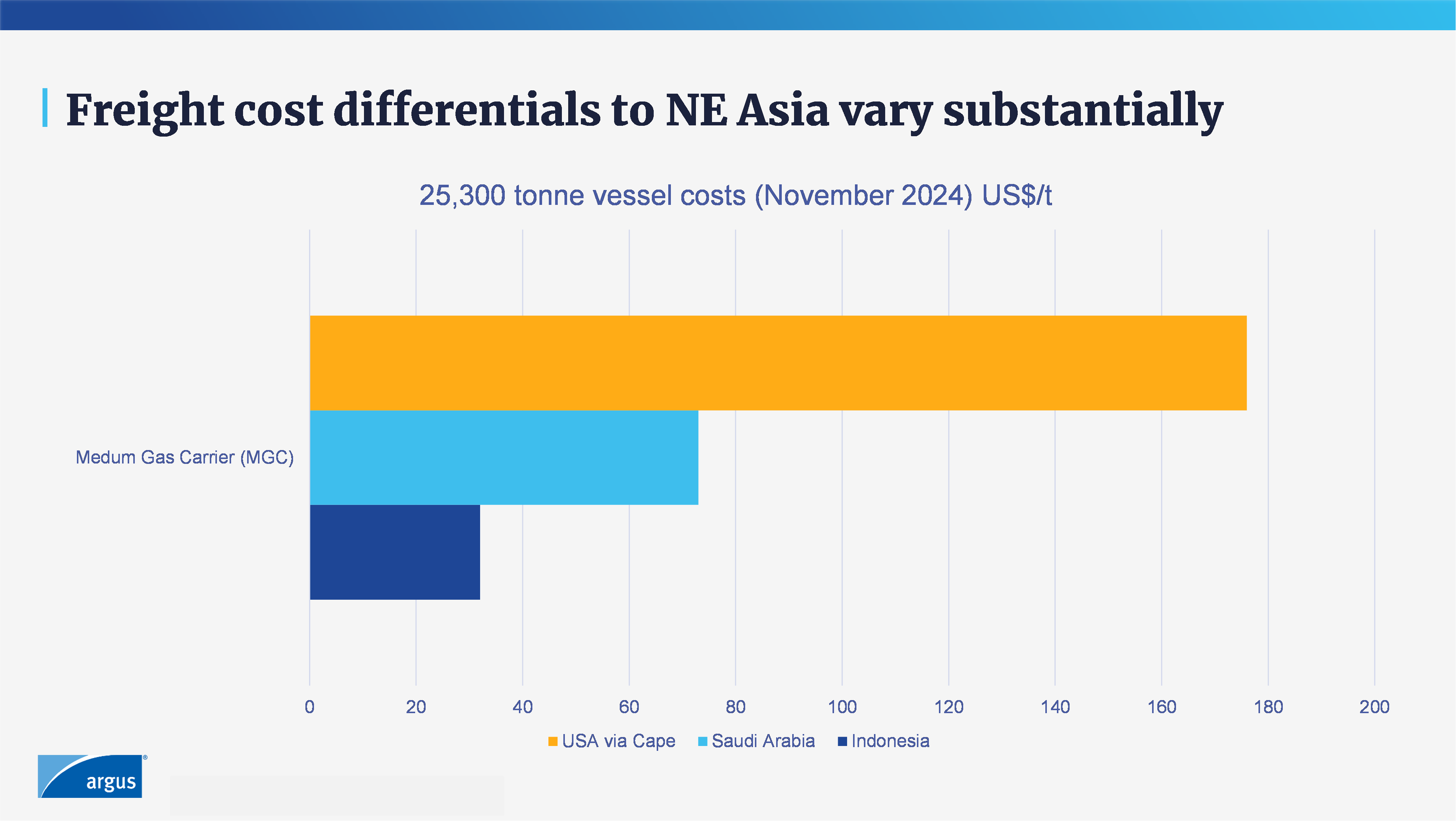

However, hydrogen will have to travel over blue water to reach Japan. Hydrogen being a diffuse gas means it will need to be bound to a ‘carrier’ molecule or liquefied, making the ammonia column charts on the right-hand side a better gauge of cost positioning.

While FOB costs vary substantially, importers like Japan must consider another cost – freight. Wide gaps between domestic production and FOB costs elsewhere mean the make or buy decision is relatively clear. Yet the travel time and outright costs of freight substantially alter the economics. The chart below captures costs that have been retreating since July, but the differentials expressed are enduring.

Taking into account the lower spread of green ammonia production costs on an FOB basis, freight is a driving criteria when considering buying from or participating in renewable ammonia projects.

Japan's Compliance Thresholds for Low-Carbon Ammonia

All renewably fed electrolytic projects will meet Japanese compliance thresholds for low-carbon ammonia. The same is not necessarily true for blue projects.

METI’s 70% emissions reduction maps onto an absolute ceiling of 0.87 tonne CO2e for each tonne of ammonia imported on a well-to-gate basis. This is a stricter definition than the initially announced gate-to-gate basis and includes upstream emissions for natural gas leakage.

For that reason and taking into account exporters’ interest in fungibility with neighboring Korea that set a 90% emissions capture requirement for natural gas-produced ammonia, autothermal reformation (ATR) projects are likely to be pursued as a ‘blue’ technology route.

Further, Japan’s expansion of the definition from gate-to-gate towards well-to-gate also pulls power consumption into the calculation, making grid carbon intensity a significant consideration for blue projects.

Challenges and Progress in Hydrogen Project Development

Security of supply is a perennial focus for Japan’s energy importers, resulting in direct investment into overseas assets.

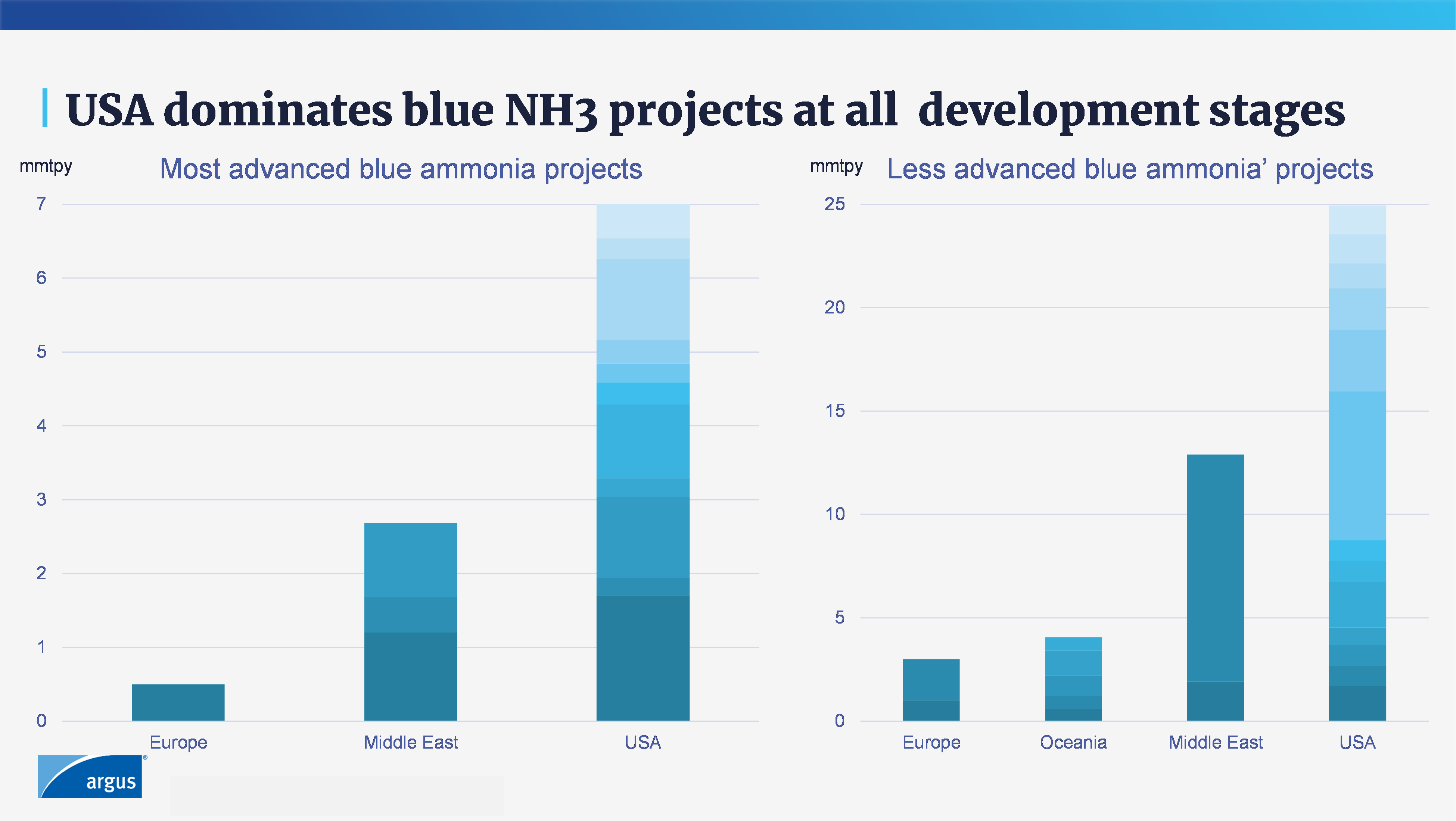

While planning for low-carbon hydrogen rules has taken centre-stage and a slew of project announcements have dominated global energy news, the last 18 months have seen snagging issues for deployment repeatedly highlighted for both blue and green projects.

Notwithstanding notable exceptions such as NEOM, a general rule-of-thumb has been that large-scale project development has skewed blue in terms of projected delivery projections.

For each of the above, it is important to look at where projects are situated and what their development stages are. The chart below displays blue ammonia projects at both more advanced stages (having agreed gas supply, or engineering and procurement or financing in place, or having groundwork/construction underway) and less advanced stages.

While the U.S. dominates both charts, it is the left-hand one that’s critical to the medium-term prospect of supply starting by 2030. Europe is in a relatively high-cost position, making supply along that time-horizon likely a North American and Middle Eastern affair.

The first chart on production costs overstates the Middle Eastern cost position, as all Argus Hydrogen and Future Fuels production costs are drawn on an equal basis from spot supply. However, a number of Middle Eastern countries offer long-term gas incentive pricing to industrial natural gas users to incentivize FDI.

This offers a quandary for such projects, who don’t want to be reduced to ‘tolling,’ but instead have a high beta with global energy prices. Yet the experience of proxy pricing in LNG has not been a fully satisfactory one, with LNG showing a low positive correlation to oil indexes. Why would ammonia (particularly the new commodity class of low-carbon ammonia) fare differently? This represents a challenge for creating binding offtakes.

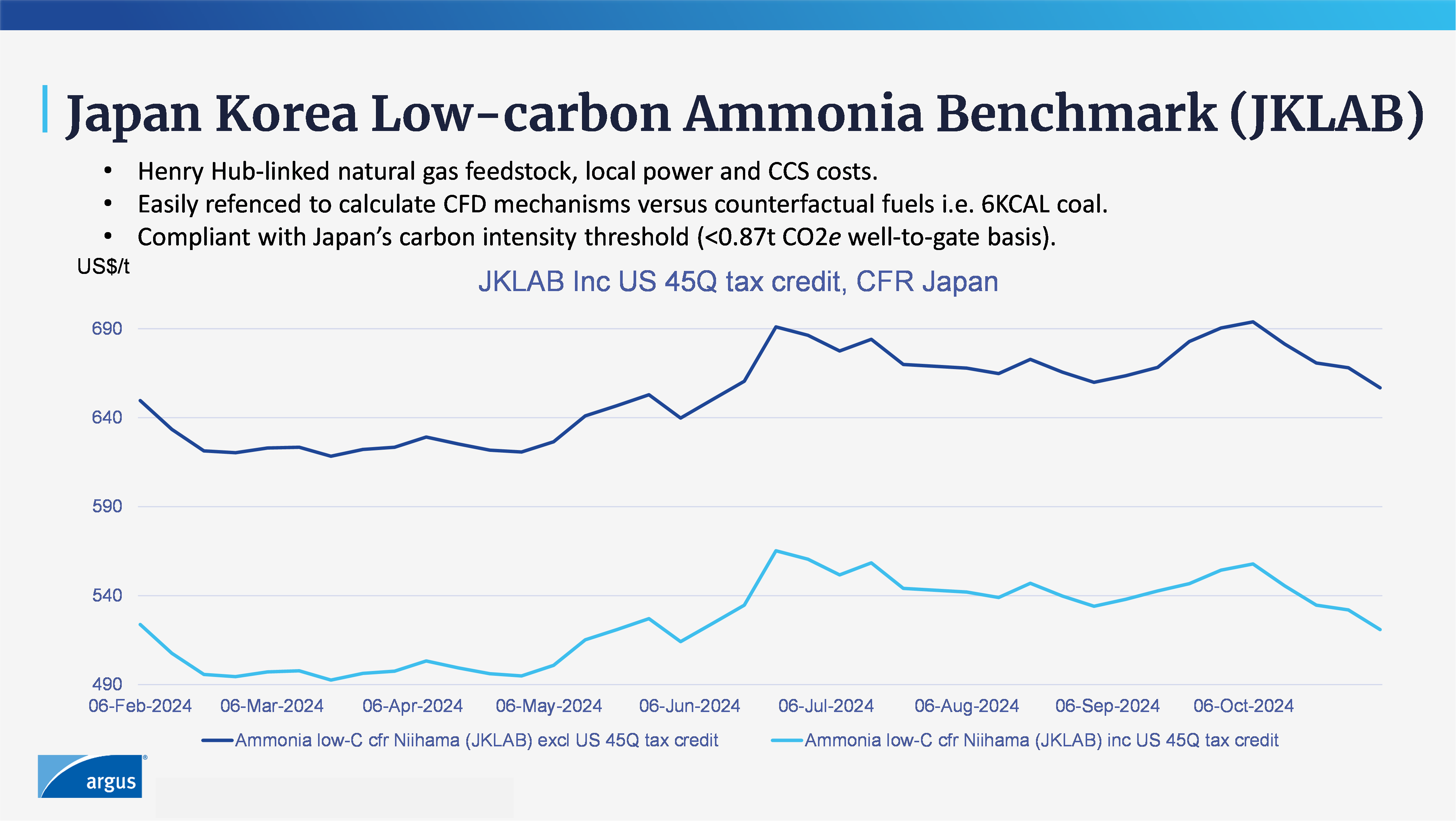

The U.S. does not share this problem. Further, it offers particularly generous support via the IRA’s 45Q provision of US$85/t of CO2 sequestered. Finally, it is leading supply-side development.

In lieu of these factors, Argus publishes the Japan Korea Low-Carbon Ammonia Benchmark (JKLAB).

The index wraps up the all-in delivered cost to both countries of world-scale blue (ATR+CCS) ammonia, including freight (the lower of Cape or Panama routes) as well as the option to include or exclude the 45Q production subsidy.

The JKLAB index creates a clear market price signal and offers the option of differential pricing to other loading locations (using freight cost adjustments). That offers an opportunity to speed up the offtake negotiation process, while also developing a uniform structure to the low-carbon ammonia and hydrogen import/export market.

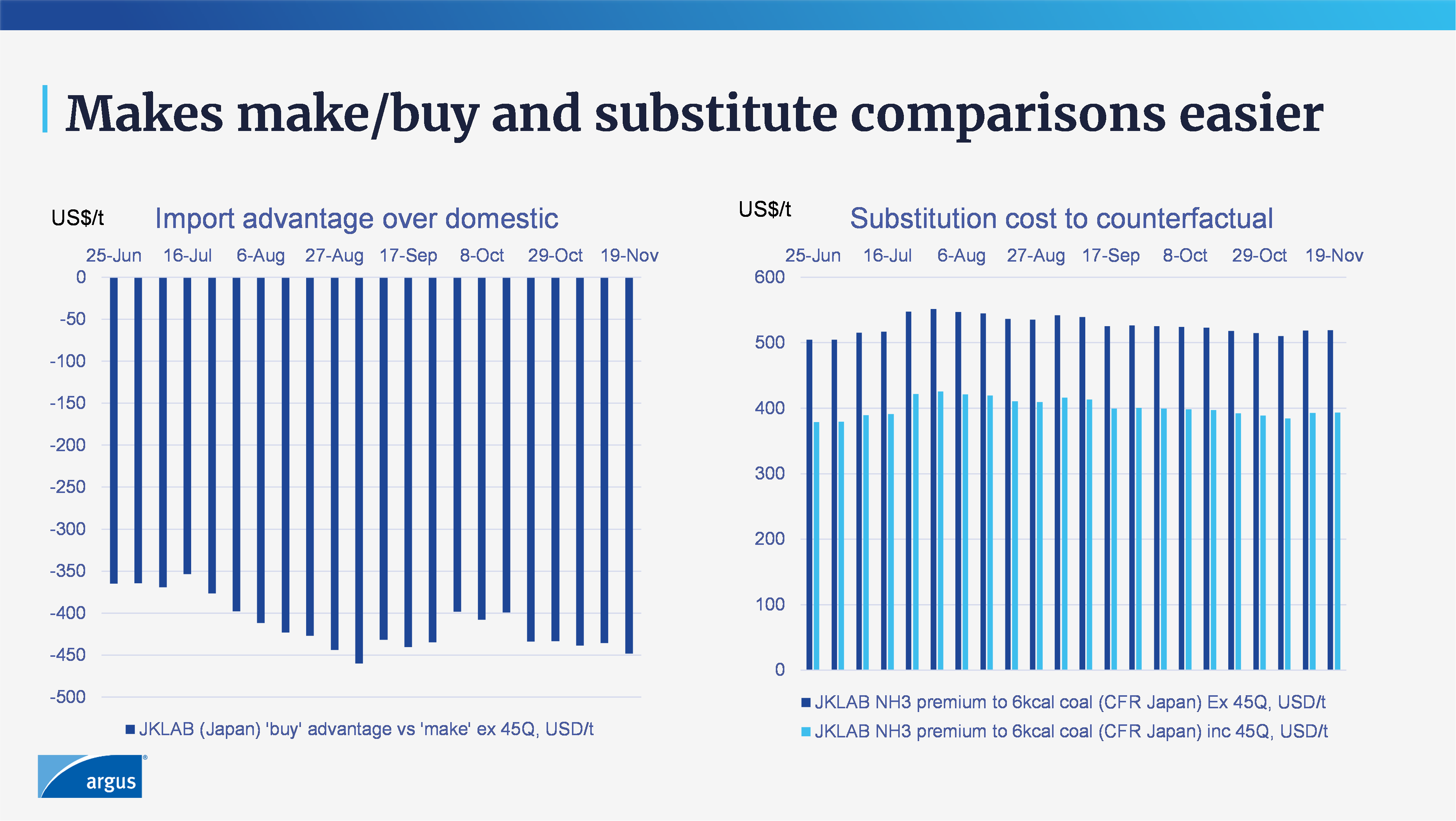

Furthermore, it makes comparisons for the make/buy decision, price gap and fossil fuel substitution costs a far easier affair.

With Japanese companies aiming to import ammonia for use in co-firing as early as 2027, there is little time to incentivize the supply-side to build capacity at scale. The signing of binding offtake-agreements is the prerequisite for that to begin.